Our goal here at Credible Operations, Inc., NMLS Number 1681276, referred to as “Credible” below, is to give you the tools and confidence you need to improve your finances. Although we do promote products from our partner lenders who compensate us for our services, all opinions are our own.

Owing money to the IRS is never fun, but it can be especially nerve-wracking when you don’t have the money to pay your tax bill.

A personal loan can be an option for paying your federal income taxes. It could also cost less in the long run than other options, like an IRS installment plan. But is using a personal loan to pay taxes the right choice for you? Here’s what to know as you consider using a personal loan to pay taxes.

Be sure to factor personal loan interest rates into your decision. You can easily view and compare personal loan rates from multiple lenders using Credible.

Should I get a personal loan to pay my taxes?

Using a personal loan to pay your taxes isn’t the right move for everyone. Personal loan lenders charge interest, and some charge origination fees ranging from 1% to 8% of the loan amount. So if you have the savings to pay your tax debt or have a cheaper borrowing alternative available, that’s likely a better way to go.

But a personal loan might be your best bet to pay your taxes if:

- You’re facing a tax bill and know you don’t have the cash to pay your balance in full (or won’t have the cash soon).

- The potential interest, penalties, and fees to set up an IRS installment agreement on your unpaid tax bill would be more than the interest and fees of a personal loan.

- You have good to excellent credit and can probably qualify for a low interest rate on a personal loan.

What happens if I can’t pay my taxes?

When you owe money to the IRS, ignoring the debt is never a good idea. The IRS charges interest and penalties on unpaid taxes, and those penalties can add up quickly if your balance goes unpaid.

Depending on your situation, you could face penalties for failing to pay your tax bill, and/or failing to file a tax return on time, and interest that compounds daily.

The IRS offers both short-term and long-term repayment plans, and you can request one by either calling the IRS at 1-800-829-1040 or by requesting a payment plan online. IRS installment plans can be convenient and are usually less expensive than paying your tax bill with a high-interest credit card. But they have their downsides.

First, penalties and interest continue to accrue until your tax bill is paid in full. If the amount you owe is high and paying it off will take several months or even years, this can significantly increase the amount you’ll pay in the end. Also, if something comes up and you can’t make a monthly payment on time, you’ll have to pay a $10 fee to revise your plan.

Both installment plans and a personal loan could help you avoid the worst-case scenario of IRS collection actions, which can include:

- Garnishing your wages

- Seizing your bank account

- Seizing other assets and selling them to satisfy the debt

- Placing a tax lien on your home or other property

- Revoking or denying you a passport

Where can I get a personal loan to pay my taxes?

A personal loan can be a good option for paying some or all your back taxes. Because they’re unsecured loans, you don’t need collateral to get a personal loan, and they’re generally widely available to borrowers with good credit.

You can find personal loans from several types of lenders, including brick-and-mortar banks, credit unions, and online lenders.

The minimum credit score needed to get a personal loan varies by lender, but many lenders will tell you upfront what their minimum requirements are. The higher your score, the more likely you are to get favorable terms, including a lower interest rate, on your loan.

In any case, it’s important to shop around for the best rate and terms available. One personal loan isn’t necessarily like another. Finding one that works for you — competitive interest rates, low fees, and affordable monthly payments — can take some time and effort, but it’s often worth it.

Credible makes it easy to compare personal loan rates from multiple lenders, without affecting your credit score.

Pros and cons of using a personal loan to pay a tax bill

Personal loans can be an appealing option for paying your taxes, but every credit product has its advantages and disadvantages, and it’s important to weigh them carefully in light of your individual circumstances.

Pros

- May be cheaper than alternatives — As of November 2021, the average interest rate on a personal loan was 9.09%, compared to 14.51% for a credit card, according to Federal Reserve data. The rates can be even higher for a cash advance on a credit card.

- You usually don’t need collateral — Personal loans are typically unsecured, so you don’t need to put your home or another asset up as collateral, as you would with a home equity loan.

- Doesn’t put your assets or property at risk — If you face financial troubles and default on an IRS installment plan, you can face IRS collections. That could mean the IRS garnishes your wages or seizes your bank account or other assets. That doesn’t happen with a personal loan.

- Manageable monthly payments — A personal loan may allow you to stretch the cost of your tax bill over multiple years, making your monthly payments more manageable.

Cons

- Taking on long-term debt — Personal loans can help you avoid IRS collections or taking on high-interest credit card debt, but they also increase your long-term debt load. This can negatively affect your credit score and increase your debt-to-income ratio, making it more difficult to get approved for other types of loans, such as a mortgage.

- Can adversely affect your credit — If you have trouble making your payments, the lender may report late and missed payments to the credit bureaus, which can lower your credit score.

- May not qualify for a low rate — If you don’t have strong credit, you could get stuck paying a higher interest rate.

- May not qualify for a large enough loan — If you have a big tax bill, it may be difficult to get a loan large enough to cover the full amount of tax you owe.

You can see your prequalified personal loan rates when you compare rates from multiple lenders with Credible.

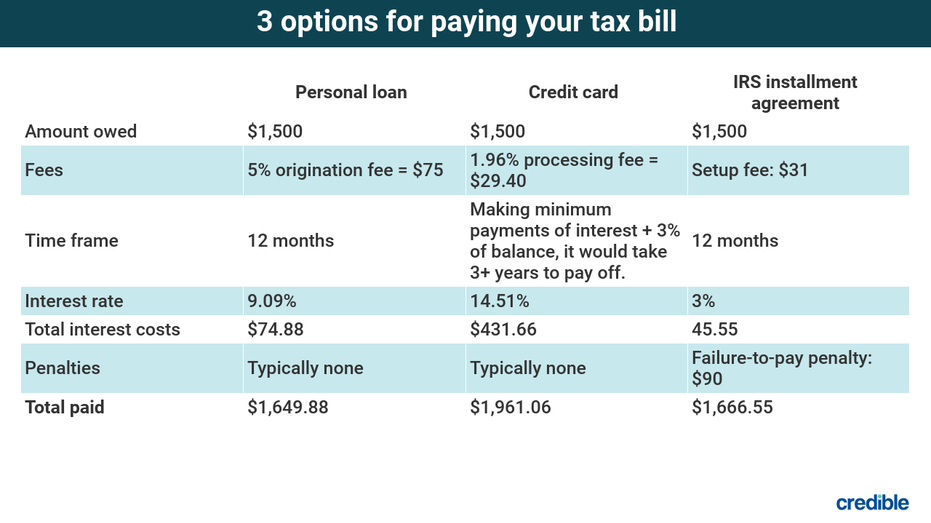

Comparing options for paying your tax bill

Personal loans aren’t the only option for paying your tax debt. Here’s a comparison of your options and how they stack up against an IRS payment plan:

Read the full article here

{kind=link}